In fintech, scaling spend without scaling measurement is how teams end up optimizing the wrong levers. The most common symptom: paid search or retargeting gets almost all the credit, while demand-driving channels “look” like they don’t convert.

In many cases, it’s not a campaign problem. It’s an attribution-model problem. In this article we’ll explain what last-click attribution is, how it works in fintech marketing, its advantages, its challenges, and when it still makes sense.

You’ll also find comparison tables, operational steps, and an actionable checklist to improve your measurement without losing control.

What is last-click attribution in fintech?

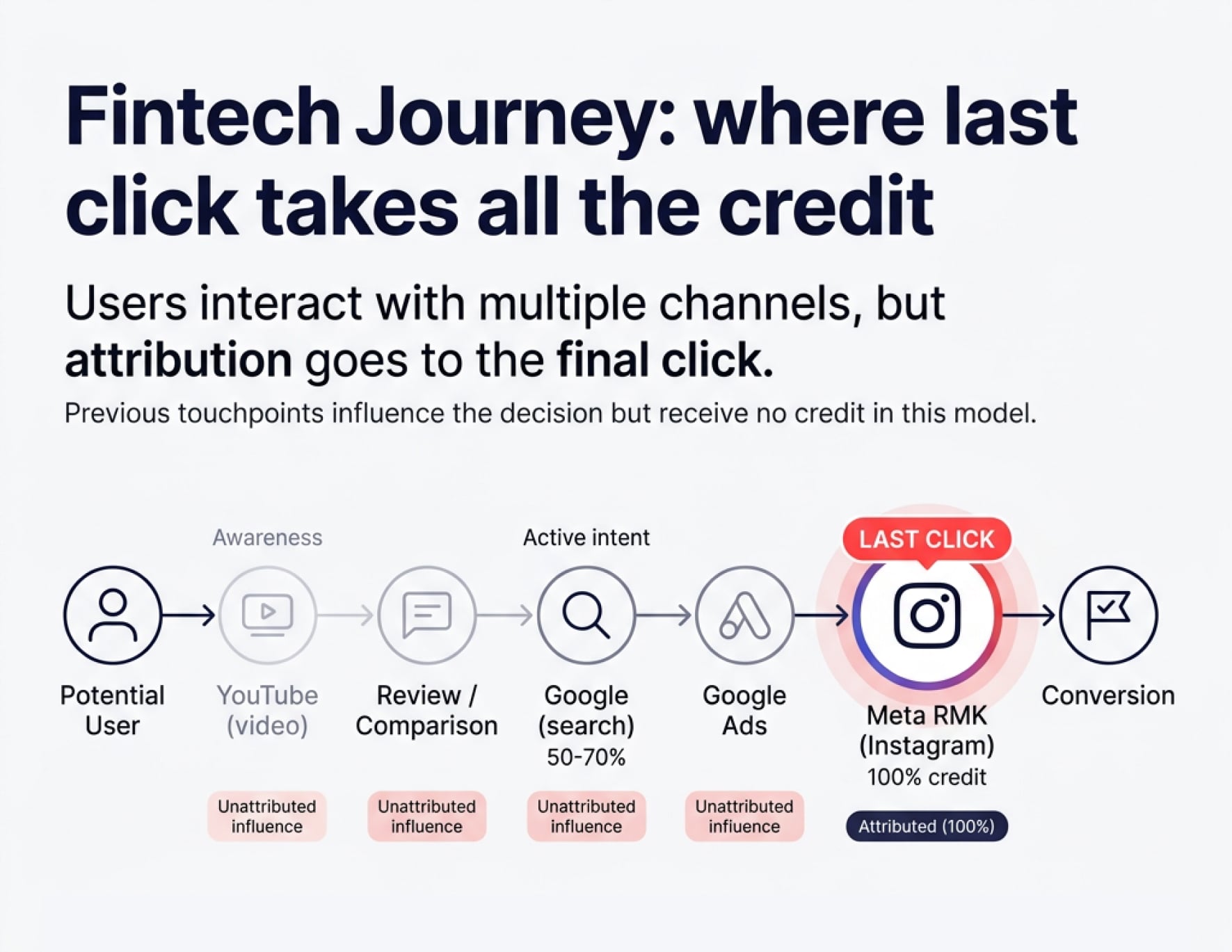

Last-click attribution is an attribution model that assigns 100% of the credit for a conversion to the last clicked touchpoint before the user converts.

In fintech, “conversion” doesn’t always mean “purchase.” It’s often a chain of milestones: signup, KYC (identity verification), first deposit, first transaction, loan approval, or card activation.

The key implication is that the model does not recognize earlier touchpoints that built intent. If a user discovers you through one channel and converts later through another, the last click takes all the credit.

What it answers (and what it doesn’t)

Last-click answers: “Which channel closed this conversion?” It does not answer: “Which channel created intent or moved the user toward the decision?”

How does the last-click attribution model work in fintech marketing?

Operationally, last-click relies on click tracking, attribution windows, and a clear definition of conversion. The model is simple, but the quality depends on your instrumentation.

Typical end-to-end steps

- Define the conversion: signup, KYC approved, first deposit, or the business event you want to optimize.

- Set up tracking (UTMs, SDKs, pixels, server-side) to capture the click that brought the user.

- Choose an attribution window: how many days after the click you will still “credit” the channel.

- Resolve identity when possible: login, user_id, hashed email to connect web + app + CRM (customer relationship management).

- Assign credit: 100% of the conversion goes to the last click within the window.

- Optimize on metrics like CPA (cost per acquisition) and ROAS (return on ad spend) for the winning channel.

Fintech example (a realistic journey)

A user sees a social ad, researches on Google, comes back through retargeting, and finally completes signup. With last-click, retargeting (or brand search) gets the credit, even if intent started earlier.

Advantages of last-click attribution in fintech

Last-click isn’t “bad” by default. It can be useful when you need a clear, operational view—especially for the closing part of the funnel.

Main benefits

- Simplicity: easy to implement and explain to business and finance.

- Tactical signal for closing: helps optimize the final step (intent capture) with fast decisions.

- Consistency: a stable baseline to compare against other models.

- Fast reporting: reduces debate when you need clear conversion ownership for weekly reviews.

When it tends to work best

It works best when the conversion happens close to the click (low latency) and when your goal is bottom-funnel efficiency. In fintech, this is more common in early growth stages or in high-intent closing campaigns.

Challenges of last-click attribution in fintech

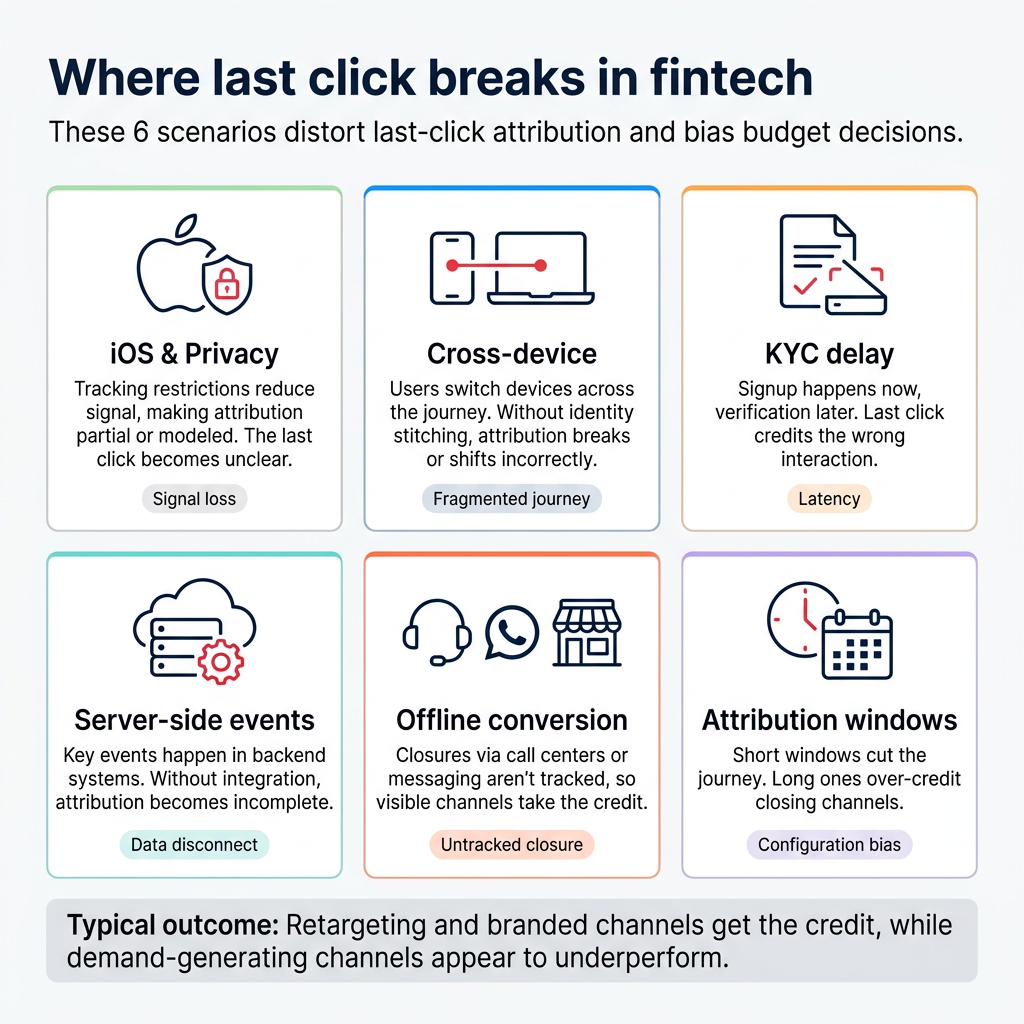

Challenges appear when the journey is long, cross-device, and constrained by privacy. In fintech, that’s the norm—not the exception.

Challenge 1: over-crediting brand and retargeting

Last-click “rewards” what closes. In practice, it can inflate brand search and remarketing, while underestimating channels that created demand.

Challenge 2: signup is not value

Many fintechs generate real value later: first deposit, first trade, or approval. If you optimize only the last click to signup, you can buy cheap volume that never reaches the business event.

Challenge 3: cross-device and multi-session behavior

Users discover in mobile, compare on desktop, and convert in app. If you don’t unify identity, credit breaks or shifts toward the last measurable environment.

Challenge 4: iOS and privacy constraints

In apps, measurement gets harder due to privacy restrictions. With SKAdNetwork (Apple’s attribution framework) and ATT (App Tracking Transparency), you lose granularity and part of attribution becomes aggregated or modeled.

Challenge 5: offline and assisted sales

If closing happens via WhatsApp, call center, branches, or manual verification and you don’t import offline conversions, the last “visible” touchpoint tends to take the credit.

Comparison table: benefits vs challenges

Below is a quick summary of where it helps and where it biases outcomes.

| Area | Benefits | Challenges |

|---|---|---|

| Simplicity | Quick setup and clear reading | Oversimplifies long, multi-touch journeys |

| Optimization | Improves closing and intent capture | Over-credits retargeting and brand |

| Management | Facilitates weekly reporting and ownership | Discourages awareness investment |

| Data | Can work with limited tracking | Degrades with privacy and cross-device loss |

| Business | Helps when conversion is near the click | May optimize “signup” instead of “value” |

First-click vs last-click attribution: which is better?

First-click attribution assigns 100% of the credit to the first touchpoint. Last-click assigns 100% to the last touchpoint. Both are single-touch: one touchpoint takes all the credit.

What each model measures best

- First-click: answers “What channel discovered me?”

- Last-click: answers “What channel closed me?”

Comparison table: first-click vs last-click

This comparison helps you choose based on the question and funnel stage.

| Criteria | First-click | Last-click |

|---|---|---|

| Best question | Origin / discovery | Closing / intent capture |

| Typical bias | Overvalues awareness | Overvalues brand and remarketing |

| Best for | Audience expansion | Bottom-funnel efficiency |

| Main risk | Ignores closing friction | Ignores demand creation |

Is last-click attribution still relevant?

Yes—but rarely as the only truth. In fintech, last-click can be a baseline and a lens for closing optimization, while the full strategy needs additional layers of measurement.

Boomit ARC Fintech model (Attribution Reality Check)

ARC Fintech is a practical framework to decide when last-click helps and what to add to avoid blind spots.

- Define your business conversion: the event that represents value (not the easiest event to track).

- Measure latency: days between first touch and that business event.

- Map signal loss: iOS, SKAdNetwork, cross-device, offline, consent.

- Choose lenses by question: closing (last), origin (first), and contribution (multi-touch where it fits).

- Validate with tests: where bias can waste budget, use incrementality tests (incrementality).

How we do it at Boomit

At Boomit we treat attribution as a system, not as a toggle in an ad platform. The goal is measurement you can trust for budget decisions—even under privacy constraints.

Practical method: data + creativity + performance

1) Value definition and events

- We choose the business event that matters (e.g., first deposit or first transaction).

- We build intermediate funnel events (signup, KYC, onboarding) to locate friction.

2) Measurement architecture

- We unify app + web + CRM (customer relationship management).

- When relevant, we integrate an MMP (mobile measurement platform) for attribution and user quality.

3) Intent-based reading (not only last touch)

- We separate demand-generation vs demand-capture campaigns.

- We diagnose bias: how much credit brand/remarketing takes vs prospecting.

4) Optimization with governance

- We use last-click as a closing lens, but we report with layers (baseline + contribution + business signals).

- We validate hypotheses with tests when bias risk is high.

Common mistakes / What to avoid

- Optimizing signup as if it were value: you end up buying cheap volume with low business impact.

- Using one lens for everything: last-click can’t answer origin and contribution at the same time.

- Not splitting brand vs non-brand in Search: brand tends to “win” last-click by definition.

- Ignoring latency: if value happens later, attribution may be cutting the journey early.

- Not bringing offline into the system: assisted sales without offline imports distort credit.

Actionable checklist

Instrumentation

- Do we have funnel events and a clear business event defined?

- Do we capture user_id or a way to unify identity once there is login?

- Do we have server-side tracking where needed (postbacks, conversion APIs)?

Attribution windows

- Does the window reflect real fintech user latency?

- Do we use different windows for signup vs business event?

Funnel and reporting

- Do we report prospecting vs remarketing separately?

- Do we split brand vs non-brand Search?

- Do we measure drop-off between signup, KYC, and first deposit?

Paid Media

- Are we reallocating budget only by last-click, or also by quality signals?

- Do we have controls to prevent remarketing from cannibalizing prospecting credit?

Privacy and apps

- Do we understand the impact of iOS/consent on our measurement?

- Are we interpreting aggregated reports correctly where applicable?

Business

- Is optimization aligned with unit economics (CAC/LTV), not only CPA?

- Do we track a post-acquisition quality KPI (e.g., % who deposit within 7/14 days)?

Conclusion + CTA: Improve your fintech campaign measurement with Boomit

Last-click attribution in fintech is still useful as a closing lens and baseline. The problem is treating it as the only truth in a world where journeys are long, multi-touch, and privacy-constrained.

If you want to scale without buying bias, the practical next step is building a measurement system that connects channels to business events. That lets you invest with more confidence and optimize for value, not just the last click.

If you want to improve attribution and performance for your fintech or digital bank, explore our Marketing Services for Fintech and Banks and share your context with us.