When you run or work at a fintech, choosing acquisition channels is not about “putting budget where the CPM (cost per thousand impressions) is cheap.” Real acquisition starts when the user trusts you, passes KYC (identity verification), and reaches a value event (first deposit, first transaction, first disbursement, first installment paid, etc.).

That’s why there is no universal ranking of “best channels.” The right channel depends on your product, friction, unit economics (CAC vs. LTV), and compliance constraints.

The good news: there are recurring patterns. And when you turn those patterns into a decision system (instead of a list of tactics), you can grow with less improvisation and less dependence on “the one channel that’s working today.”

What Are Acquisition Channels in Marketing?

An acquisition channel is the path through which a person discovers your product and enters your funnel until completing an action that truly matters to the business.

In fintech and banking marketing, that action is rarely just “sign-up.” What really matters is the event that confirms intent + quality + monetization potential.

To avoid common confusion, it helps to separate:

- Channel: Search, Social, Affiliates, Partnerships, Referrals, etc.

- Tactic: Retargeting, lookalikes, lead ads, UGC (user-generated content).

- Metric: CAC (customer acquisition cost), CPA (cost per acquisition), CVR (conversion rate), ROAS (return on ad spend), LTV (lifetime value).

If your team calls everything a “channel,” you’ll end up comparing apples to oranges and allocating budget without real criteria.

Why Is It Critical to Define Acquisition Channels Correctly in Fintech?

Because fintech has two invisible costs that many teams discover too late: trust cost and friction cost.

You can buy traffic, but you can’t buy trust with a weak ad. And you can generate registrations, but if your funnel breaks at KYC or activation, you’re just paying for users who never reach value.

On top of that, fintech acquisition is deeply shaped by compliance and reputational risk. That affects ad copy, landing pages, and partner selection. This isn’t a “legal detail”; it’s a performance variable.

In short, defining channels properly helps you make better decisions across three dimensions:

- What type of demand to capture (intent vs. discovery)

- Which event to optimize for (registration vs. KYC vs. activation)

- What risk to accept (fraud, claims, dependency, cohort quality)

There’s no single recipe, but there is a set of channels that consistently perform when executed with discipline. Below are the main acquisition channels for fintech—when they make sense, what to measure, and what to watch out for—without turning this into an endless inventory.

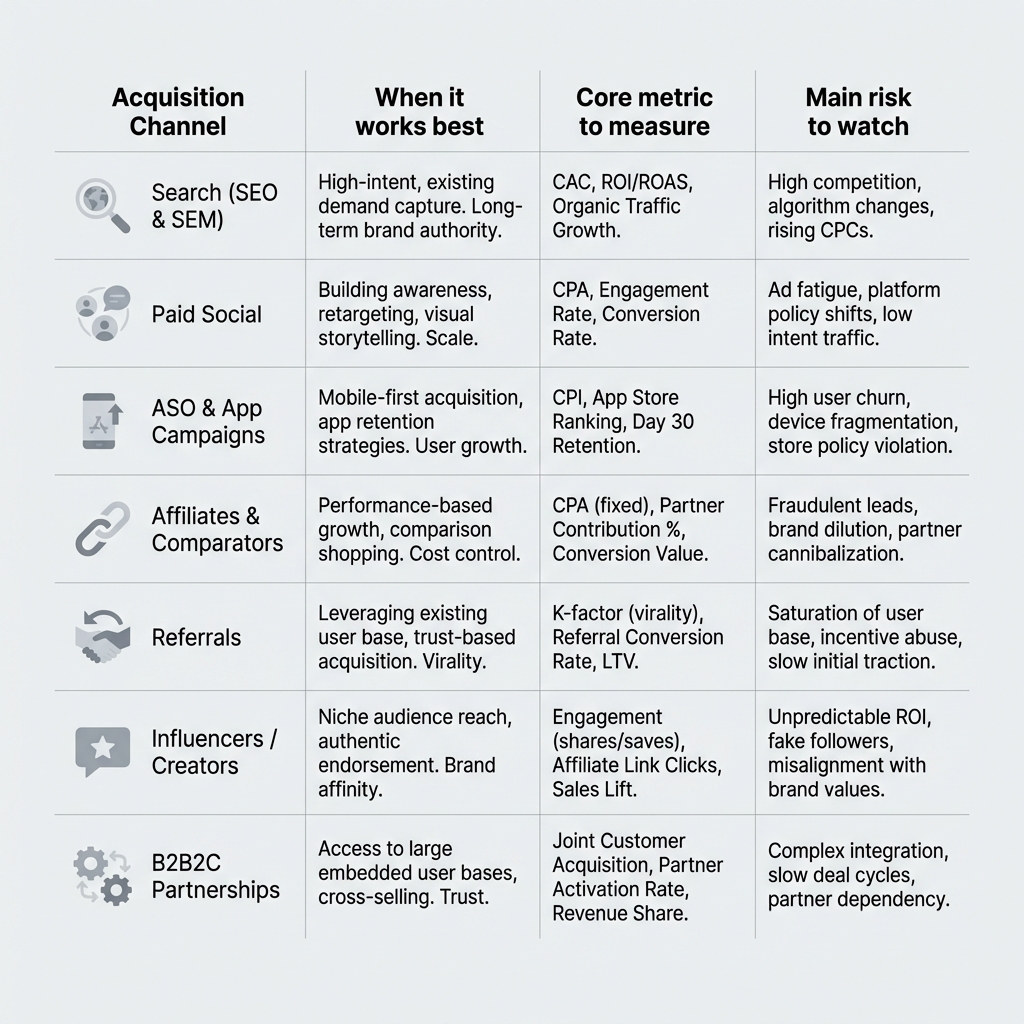

1. Search (SEO + SEM)

Search is often the most reliable engine when there is explicit intent. If someone searches for “personal loan,” “no-fee account,” or “travel credit card,” they’re already close to a decision. Your job is to show up, explain conditions clearly, and convert.

When it works best

- Categories with active demand and comparable offers.

- When you can segment by real intent (not all keywords are equal).

What to measure (beyond clicks)

- CPA/CAC by intent (brand vs. non-brand).

- % of approved KYC and post-KYC activation.

- Cohorts by keyword or ad group (quality, churn, revenue).

What to watch out for

- Landing pages with clear, consistent conditions.

- “Clean” messaging: what you promise in ads must hold true in the product.

2. Paid Social (Meta / TikTok / LinkedIn)

Paid Social works well for demand creation, especially when users aren’t actively searching yet. In fintech, this is critical: many users don’t “need” your product until they understand why it benefits them or why they should trust you.

Success here isn’t just targeting—it’s creative + clarity. Your creative is your salesperson in the first two seconds.

When it works best

- Fast scale and message/angle testing.

- When your differentiation can be shown with examples: control, transparency, benefits, experience.

What to measure

- CPA by funnel stage: registration / KYC / activation.

- Payback or ROAS, depending on your model.

- Cohort quality (not just volume).

What to watch out for

- Risky claims and absolute promises (performance and reputation killers).

- “Pretty” creatives with no intent—clarity usually wins in fintech.

3. ASO + App Campaigns (If You’re App-First)

If your product lives on mobile (wallets, payments, investing), acquisition doesn’t end at install. Apps can easily inflate installs and still fail due to low activation.

That’s why smart teams optimize for value-correlated events, not CPI.

When it works best

- Mobile-first products with relatively short time-to-value.

- When your store listing reduces friction and sets expectations.

What to measure

- CPE (cost per event) for approved KYC, first deposit, first transaction.

- D7/D30 retention by source.

- Quality signals (fraud, chargebacks if relevant).

What to watch out for

- Onboarding friction: every extra step burns money.

- Clear event definitions for proper optimization.

4. Affiliates and Comparison Sites (Performance Partnerships)

Affiliates work well when users are in evaluation mode, comparing options and conditions. In fintech, they can be very efficient—but also risky if messaging and incentives aren’t controlled.

When it works best

- Comparable offers (rates, fees, benefits) with clear value propositions.

- When you need to diversify acquisition beyond paid ads.

What to measure

- CAC by partner and quality (KYC pass rate, activation, retention).

- Result concentration (over-reliance on one partner = risk).

What to watch out for

- Compliance of partner content.

- Incentives that attract “bonus hunters” instead of valuable users.

5. Referrals and Product Loops

Referrals are powerful when the product has a social component or delivers an experience users genuinely want to recommend. In fintech, done right, this can be one of the most efficient channels. Done wrong, it becomes an abuse factory.

When it works best

- P2P, payments, wallets, and network-effect products.

- When incentives align with real value, not just sign-ups.

What to measure

- Net CAC and activation of referred users.

- K-factor (virality coefficient), with strong fraud monitoring.

What to watch out for

- Anti-abuse rules from day one (limits, validations, patterns).

- Incentives tied to value events (deposit/transaction), not registration.

6. Financial Influencers / Creators (Performance-Driven)

Creators provide something ads often can’t: borrowed trust and contextual explanation. For fintech, this is extremely valuable—if messaging is guided and cohorts are measured.

When it works best

- Products that require education (investing, credit, insurance).

- When you can track performance via links/codes and compare cohorts.

What to measure

- CAC per creator + quality (KYC, activation).

- Brand search lift and direct traffic as trust signals.

What to watch out for

- Compliance-approved messaging and proper disclaimers.

- Avoid hype-driven influencers; prioritize real performance and fit.

7. B2B2C Partnerships (Distribution)

When a partner lends you distribution and trust (employers, retailers, telcos, ecosystems), the economics can change entirely. The trade-off: cost isn’t always media—it’s integration, revenue share, and operations.

When it works best

- High direct CAC models or categories with high trust requirements.

- Embedded finance (payroll, embedded credit, benefits).

What to measure

- Total CAC (including integration + revenue share).

- Conversion and time-to-value by partner cohort.

What to watch out for

- Over-dependence on a single partner.

- Poor data integration and lack of funnel visibility.

How to Choose the Right Acquisition Channels for Your Fintech

Many companies choose channels based on trends or competitor behavior. Instead of choosing by fashion, choose by diagnosis. The right decision almost always comes from answering two questions:

What is my value event?

How expensive is trust in my category?

1) Define your value event (don’t marry the sign-up)

Typical examples:

- Lending: Approved KYC + disbursement (then first installment paid).

- Wallets/Payments: First deposit + first transaction.

- Investing: First deposit + first trade.

- Accounts: First transfer or average balance (model-dependent).

Build campaigns and dashboards around that event—not a proxy.

2) Map friction and trust

A quick mix guide:

- High intent + high trust → Search + SEO/content + creators + clear landings.

- Low intent + high trust → Paid Social + social proof + partnerships.

- High intent + low friction → Search + ASO + affiliates.

- Low intent + high virality → Social + referrals + product loops.

3) Prioritize by stage

- 0→1: Two core channels (intent + discovery) and fast learning.

- 1→10: Double down on what works + one diversification channel.

- 10→100: Efficiency via SEO, performance content, lifecycle, automation.

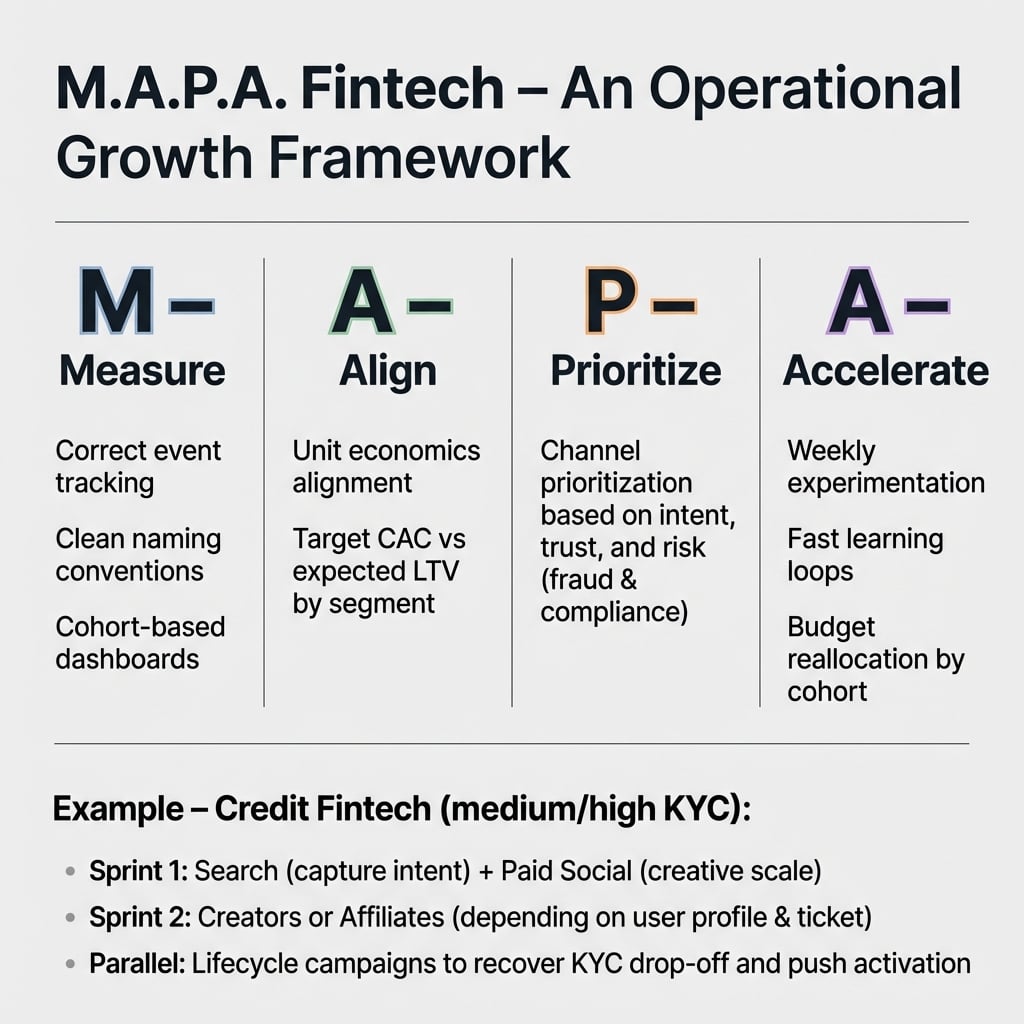

How We Do It at Boomit

We use a simple, operational framework—not PowerPoint strategy.

Boomit Framework: M.A.P.A. Fintech

- Measure the right event: tracking, naming, cohort-based dashboards.

- Align unit economics: target CAC vs. expected LTV by segment.

- Prioritize channels: intent + trust + risk (fraud/compliance).

- Accelerate learning: weekly experimentation and cohort-based budget reallocation.

We run this in sprints. For example, in a credit fintech (medium/high KYC), we typically start with Search to capture intent, add Paid Social for creative scale, and in the second sprint test creators or affiliates based on user profile and ticket size. In parallel, we activate lifecycle to recover abandoned KYC and push activation.

Common Mistakes / What to Avoid

The #1 fintech acquisition mistake is optimizing for the easiest metric to inflate. Cheap registrations are a trap when your business lives in KYC and activation.

Other recurring mistakes:

- Relying on a single channel (when it drops, everything drops).

- Risky claims that landing pages or support can’t sustain.

- Unaudited affiliates (low quality or compliance risk).

- Ignoring cohorts: averages lie, segments tell the truth.

Actionable Checklist

To turn this into a plan, check if you have:

- A defined value event (KYC/activation) with end-to-end measurable funnel.

- Stage-level KPIs: CPA/CAC + progression rates (sign-up → KYC → activation).

- Cohorts by source (keyword/audience/partner/creator), not just totals.

- Clear, compliance-ready messaging and landing pages.

- Two core channels selected (intent + discovery).

- One diversification channel planned (affiliates/creators/partners).

- Active lifecycle flows to recover abandoned KYC and accelerate activation.

- Weekly experimentation rhythm (3–5 tests) with quality-based decisions.

Conclusion

The acquisition channels that tend to work best in fintech combine three elements: intent capture (Search/SEO), creative scale (Paid Social/Creators), and trusted distribution (Partnerships/Affiliates/Referrals). The right order depends on your friction (KYC), value proposition, and unit economics (CAC vs. LTV).

If you want, at Boomit we can help you design an acquisition mix with solid measurement and weekly experimentation—focused on users who activate, not just leads. Learn more about our Marketing Services for Fintech and Banking.