Reducing CAC (Customer Acquisition Cost) in fintech is not about “cutting budget” or fighting for cents on CPM (cost per thousand impressions). It goes much deeper than that. It’s a system-level problem: improving signal, conversion, activation, and customer quality so that every dollar invested brings users who actually use the product and generate value.

In fintech, this is even more delicate because the funnel has unavoidable friction (KYC, validations, risk checks, regulation). That’s why optimizing “too high up” the funnel (for example, for registrations) may make CAC look lower—while the business sees no real impact.

What Is Customer Acquisition Cost (CAC) and Why Is It Critical in Fintech?

Let’s start with the basics.

CAC (Customer Acquisition Cost) is the average cost of acquiring a new customer. The basic formula is simple:

.

The trap lies in defining what “customer” means in fintech. In most cases, the real customer is not someone who registers—but someone who passes KYC and activates.

In practice, CAC should be analyzed at different levels, because each stage tells a different story:

- CAC per registration (useful for volume, but misleading)

- CAC per approved KYC (KYC = Know Your Customer, identity verification)

- CAC per activation/funding (first deposit, first purchase, first transfer or first transaction, depending on the product)

Why does this matter so much in fintech? Because growth is only sustainable if LTV (Lifetime Value) justifies CAC. If CAC goes down in your dashboard but activation or quality drops, LTV won’t follow—and growth becomes expensive and unstable.

Main Challenges When Reducing CAC in Fintech

Most teams try to reduce CAC by tweaking campaigns (bids, audiences, budgets). But in fintech, issues are usually spread across measurement, funnel and product. That’s why CAC keeps rising even when paid media “looks right”.

The most common challenges repeat themselves:

- Optimizing for the wrong events: focusing on registrations when unit economics depend on KYC and activation.

- Incomplete tracking: broken attribution between web and app, missing deduplication, weak signals for ad platforms.

- Onboarding friction: long flows, KYC errors, unclear next steps.

- Audience saturation: same targeting, same message, same offer → CPM goes up, CTR goes down.

- Low lead quality: users who don’t qualify (credit), don’t fund or never return.

- Generic creatives: talking about “the app” instead of the user’s real problem.

The key point: this is not solved with a single lever. It requires coordinated moves.

3 Effective Strategies to Reduce CAC in Fintech Without Slowing Growth

Below are three strategies that have consistently worked with our clients.

Strategy 1: Reduce CAC by Increasing Real Conversion (Pre- and Post-Click), Stage by Stage

In fintech, the click is just the beginning. Real conversion happens when users overcome friction and reach activation. Improving mid-funnel conversion often reduces CAC more than any media-buying optimization.

Think in terms of the full funnel.

.

Actions that usually drive fast impact:

- Define “customer” by stage and report CAC per stage (registration / KYC / activation).

- Align ads with landings/app stores: if you promise “no-fee card,” that must be the first thing users see—clearly and honestly.

- Reduce first-minute friction: direct microcopy (“takes X minutes,” “you’ll need an ID”), no unrealistic promises.

- Run disciplined CRO: one variable per test (headline, field order, verified social proof, error messages).

- Guide activation: onboarding checklists and contextual nudges (“only one step left”).

Here, the most useful metric is not overall conversion rate, but CVR by stage: click→registration, registration→KYC, KYC→approval, approval→activation. When an expensive stage improves, CAC drops without changing budget.

Strategy 2: Optimize for Value (LTV) and Customer Quality, Not Just CPA

The classic mistake is optimizing for CPA (Cost per Acquisition) as if all acquisitions were equal. In fintech, the “cheap customer” can be the most expensive one if they never activate, qualify or generate margin.

The correct approach is to optimize toward value—ideally LTV, or value proxies if LTV is not yet available.

How to execute this in practice:

- Build cohorts by channel/campaign and track % approved KYC, % activation, D7/D30 retention and ARPU (Average Revenue Per User).

- Assign value weights to mid-funnel events when LTV isn’t consolidated yet (values depend on internal economics):

- Approved KYC = value 1

- First deposit = value 3

- Second transaction = value 5

- Import backend conversions (server-side): stronger signals, less pixel dependency, better optimization.

- Remove structurally bad segments: if a segment always fails KYC or never funds, exclude it or change the offer.

The KPIs that bring order here are CAC per activated customer and payback by cohort (days to recover CAC). This is how you avoid “fake efficiency.”

Strategy 3: Creativity + Offer + Job-Based Segmentation (Not Demographics)

When CAC rises, many teams obsess over targeting. But in low-signal, high-competition environments, the real advantage is the triangle: message + offer + creativity.

In fintech, users don’t buy “an app”—they buy an outcome. Typical jobs include:

- “I want to organize my finances without wasting time.”

- “I need clear, transparent credit.”

- “I want to invest without feeling scammed.”

- “I want to pay and get paid more easily than with a bank.”

Turn those jobs into a creative system:

- Creative pillars per job + objection (e.g., easy investing + fear of losing money).

- Offers with controlled friction: often better to incentivize activation, not registration.

- Demo/UGC creatives showing the real flow: registration → KYC → first use.

- Stage-based remarketing: tailored messages for KYC started, funding abandoned, credit simulated, etc.

Measure with a dual lens: CTR for message relevance and post-click CVR for onboarding consistency. If CTR goes up but CVR drops, your promise isn’t matching the product experience.

How to Measure and Optimize CAC Reduction in Fintech

To make CAC reduction real—not an illusion—measurement must reflect business outcomes.

Recommended KPIs:

- CAC per registration / approved KYC / activation

- CPA for critical events

- CVR by funnel stage

- Payback by cohort

- D7/D30 retention

- ROAS only if monetization is immediate; otherwise prioritize payback + LTV proxies

Operating cadence that works:

- Daily: campaign health, spend, frequency, tracking

- Weekly: performance by cohort and stage

- Bi-weekly: controlled experiments (creative, offer, CRO)

- Monthly: acquisition channel mix and attribution review

Simple rule: never celebrate low CAC if activation drops or payback worsens.

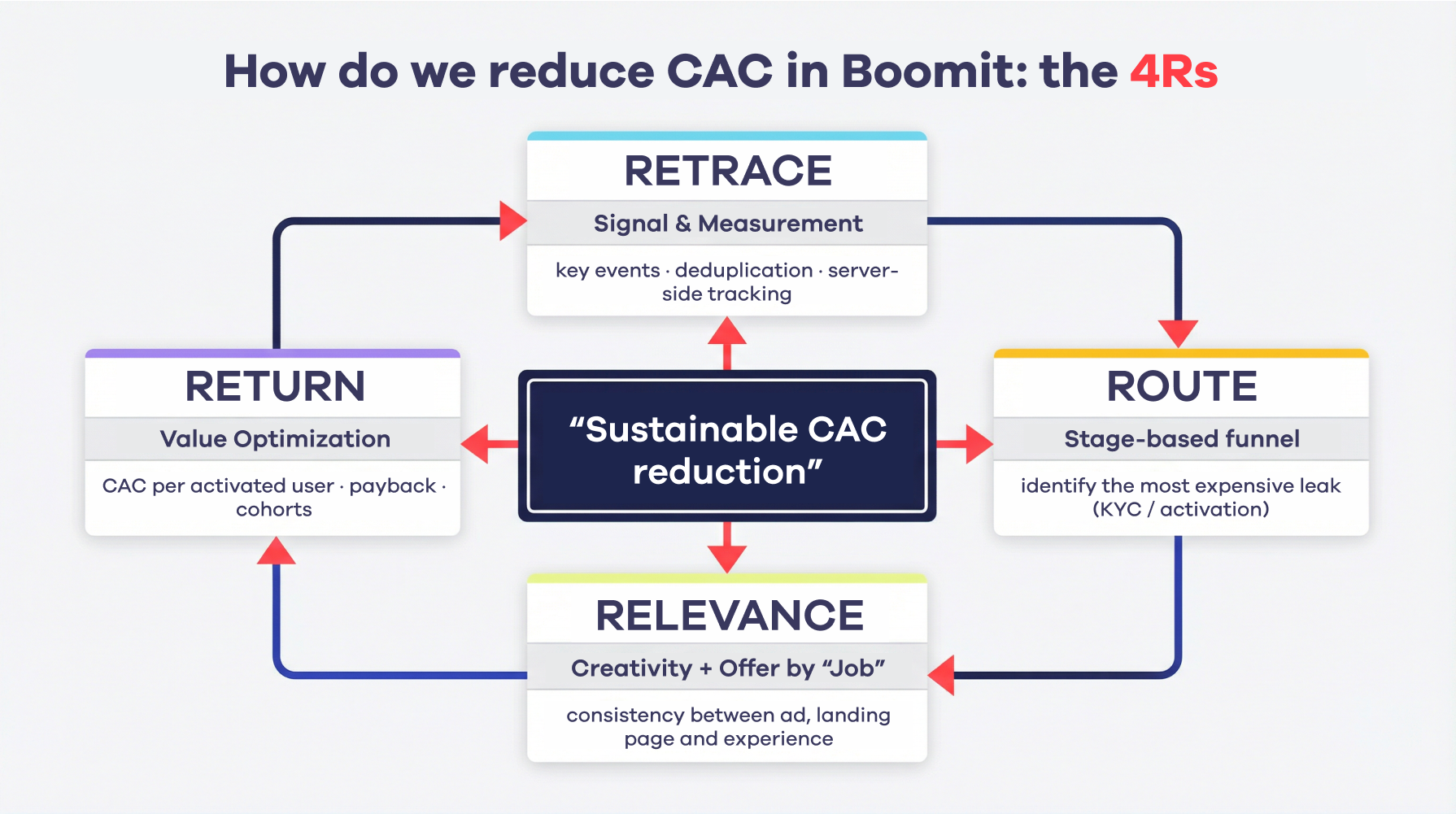

How We Do It at Boomit

At Boomit, we treat CAC reduction as a connected machine—not isolated campaigns. Sustainable CAC reduction happens when signal, funnel, creativity and value work together. A simple way to remember it is the 4 Rs:

.

1) Retrace (Signal & Measurement)

Solid instrumentation, key events, deduplication and server-side tracking when needed.

2) Route (Stage-Based Funnel)

We map the full journey and prioritize the most expensive leak—often KYC or activation.

3) Relevance (Creativity + Offer by Job)

Clear, honest creatives aligned with what users experience after the click.

4) Return (Value Optimization)

From volume to quality: CAC per activated user, payback and cohorts.

Common Mistakes / What to Avoid

- Optimizing for registrations when the business depends on KYC and activation

- Changing too many variables at once

- Overpromising what the product can’t deliver

- Ignoring onboarding

- Making decisions only from ad platform dashboards

- Burning out winning creatives through saturation

Actionable Checklist

- Define customer by stage and report CAC by stage

- Implement key events and deduplication

- Measure CVR by stage

- Run CRO tests focused on the biggest leak

- Optimize media toward value-adjacent events

- Build stage-based remarketing

- Define creative pillars by job

- Analyze cohorts and payback

- Define value proxies if LTV is not available yet

Conclusion

Reducing CAC in fintech is a multi-variable problem: signal quality, friction reduction, job-aligned creativity and value-based optimization (LTV), not just CPA. When these pieces align, CAC drops without slowing growth.

If you want, at Boomit we can help you identify the most expensive funnel leak, clean up measurement and design an experimentation plan to reduce CAC with quality control and clear payback—through our Marketing Services for Fintech and Banking.